.jpg)

We've compared the leading FinFit alternatives for 2026, including Origin, Bank of America Workplace Benefits, YNAB, and SmartDollar, with Your Money Line standing out as the top solution. Unlike product-driven platforms, Your Money Line delivers a truly comprehensive financial wellness experience: personalized for every employee, backed by certified financial coaches, and designed to eliminate the root cause of financial stress, not just manage its symptoms.

FinFit positions itself as an employee financial wellness solution built around access to money, combining payroll-linked savings, emergency credit, and personal loans to create what it calls a "financial safety net." For organizations where short-term liquidity is the most pressing need, it can serve as a starting point. But a safety net, by design, catches you after you fall. It doesn't teach you how to walk the tightrope.

Think about how we approach physical health at work. When an employee gets sick, we don't simply hand them a prescription and send them on their way, we invest in preventive care, annual checkups, and wellness programs that keep them healthy before a crisis hits. Because every HR leader knows the truth: reactive healthcare is far more expensive than proactive healthcare. The emergency room costs more than the annual physical. Surgery costs more than the lifestyle changes that could have prevented it. And perhaps most painfully, treating a symptom without addressing its root cause almost guarantees the problem comes back and often worse than before.

Financial wellness works exactly the same way.

When employees are living paycheck to paycheck, the instinct is to hand them a financial prescription: a loan, a line of emergency credit, early access to wages they haven't yet earned. And like the ER visit, that prescription can feel like a lifesaver in the moment. But if the underlying cause, no budget, no savings habit, no financial roadmap, is never addressed, the next emergency is already on its way. And the one after that. Each short-term fix leaves employees with a little less financial cushion than before, making the next crisis more likely, not less.

This is the fundamental problem with platforms built around lending and credit access as the centerpiece of financial wellness. They treat the symptom. They don't cure the disease. And for HR leaders evaluating financial wellness benefits on a tight budget and a tight timeline, the "low-cost, low-commitment" appeal of a product-driven platform can be genuinely enticing, until you realize that the cost isn't just the licensing fee. It's the turnover, the absenteeism, the lost productivity, and the compounding financial stress of a workforce that keeps needing the ER because no one ever helped them get healthy in the first place.

The most effective financial wellness solutions address the full picture: budgeting, debt, savings, retirement, and everything in between, without steering employees toward financial products that may deepen the very stress the benefit was meant to relieve. They're the annual physical, not the emergency room. They're proactive, not reactive.

The numbers are hard to ignore. According to Your Money Line's 2026 Employee Financial Behavior Report, 62.48% of employees say financial stress has a major or moderate impact on their focus and productivity at work, and nearly seven in ten (68.61%) are actively considering a job change or reducing their work hours as a result.

The encouraging news? Employees are more open to support than ever. Nearly three in four (72%) employees say they would likely use financial coaching or wellness tools if their employer offered them.

The challenge is that today's workforce spans multiple generations with different financial starting points, different spending pressures, and different levels of financial literacy. What an hourly worker needs at 25 looks nothing like what a mid-career employee needs at 45. And neither of them will be well-served by a platform whose primary answer to financial stress is: "here's a loan."

FinFit tends to be best for organizations that:

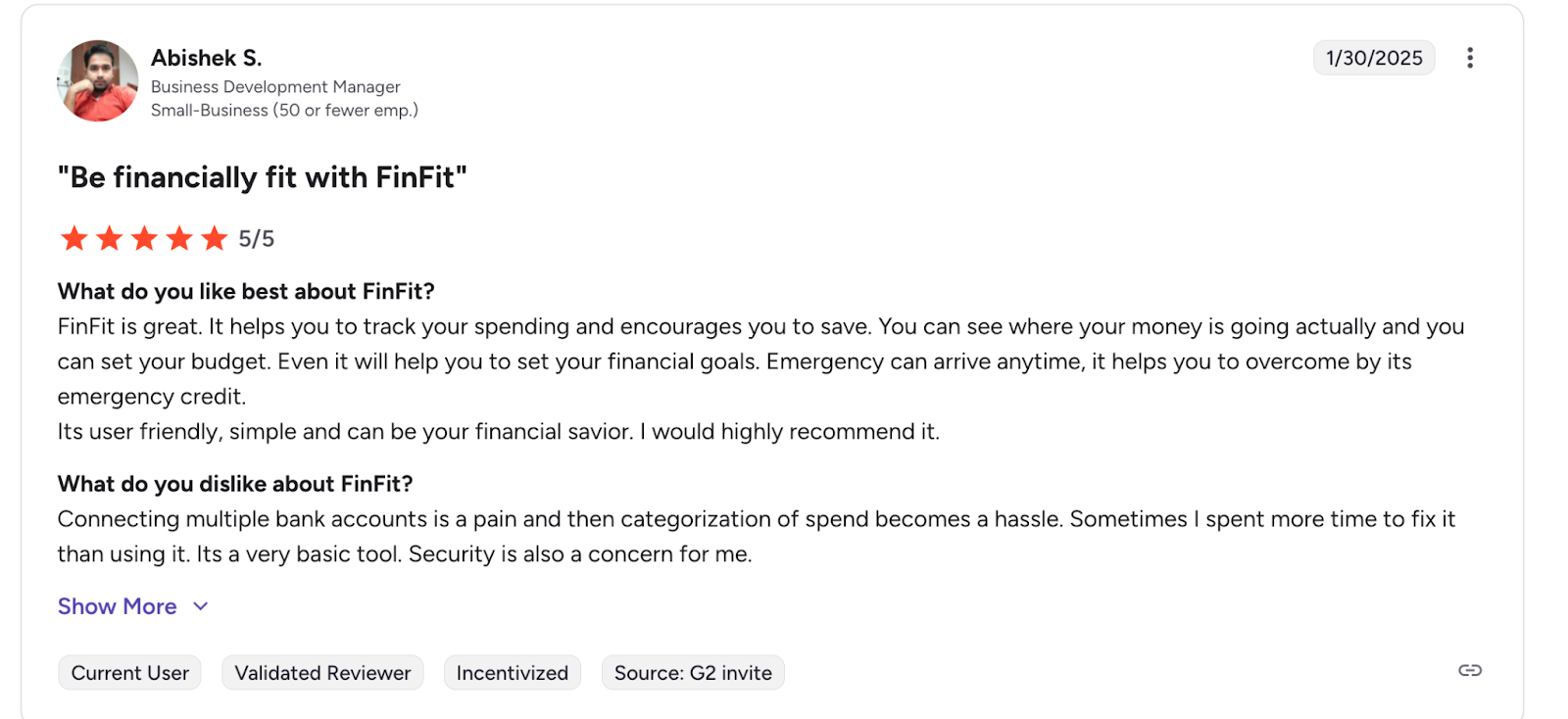

FinFit may work for some organizations. Its freemium base layer is easy to implement, and for employees facing a genuine short-term cash crisis, the platform's emergency credit and loan offerings can feel like a lifeline. But here's what that framing misses: an employee who needs a loan today and takes one out through FinFit will have less money in their next paycheck. That smaller paycheck increases the odds that they'll need another loan next month. And the month after that.

It's worth noting that FinFit does offer tools beyond lending, budgeting dashboards, financial assessments, and education content are all part of the platform. But in practice, those tools exist alongside a business model built around credit and loans, and that tension is hard to resolve. When the core product is a financial lifeline, the educational layer becomes secondary, something employees may never meaningfully engage with because the path of least resistance is always the loan.

This isn't a criticism of employees, it's a criticism of a model. When the business is built around lending, the platform succeeds when employees borrow. That's a structural conflict of interest that no amount of budgeting content or financial education can fully offset.

For HR leaders, the distinction matters enormously, not just philosophically. The real cost of financial stress isn't measured in benefits spend. It's measured in turnover, absenteeism, distracted employees, and healthcare costs tied to stress-related illness. A benefit that treats the symptom without addressing the root cause doesn't reduce those costs. It defers them.

The question every HR leader should be asking isn't "what does this benefit cost per employee per year?" It's: "Is this benefit actually making my employees more financially stable, or is it just making them more comfortable being financially unstable?"

Users have noted that connecting multiple bank accounts can be cumbersome, and categorizing spending becomes time-consuming to manage.

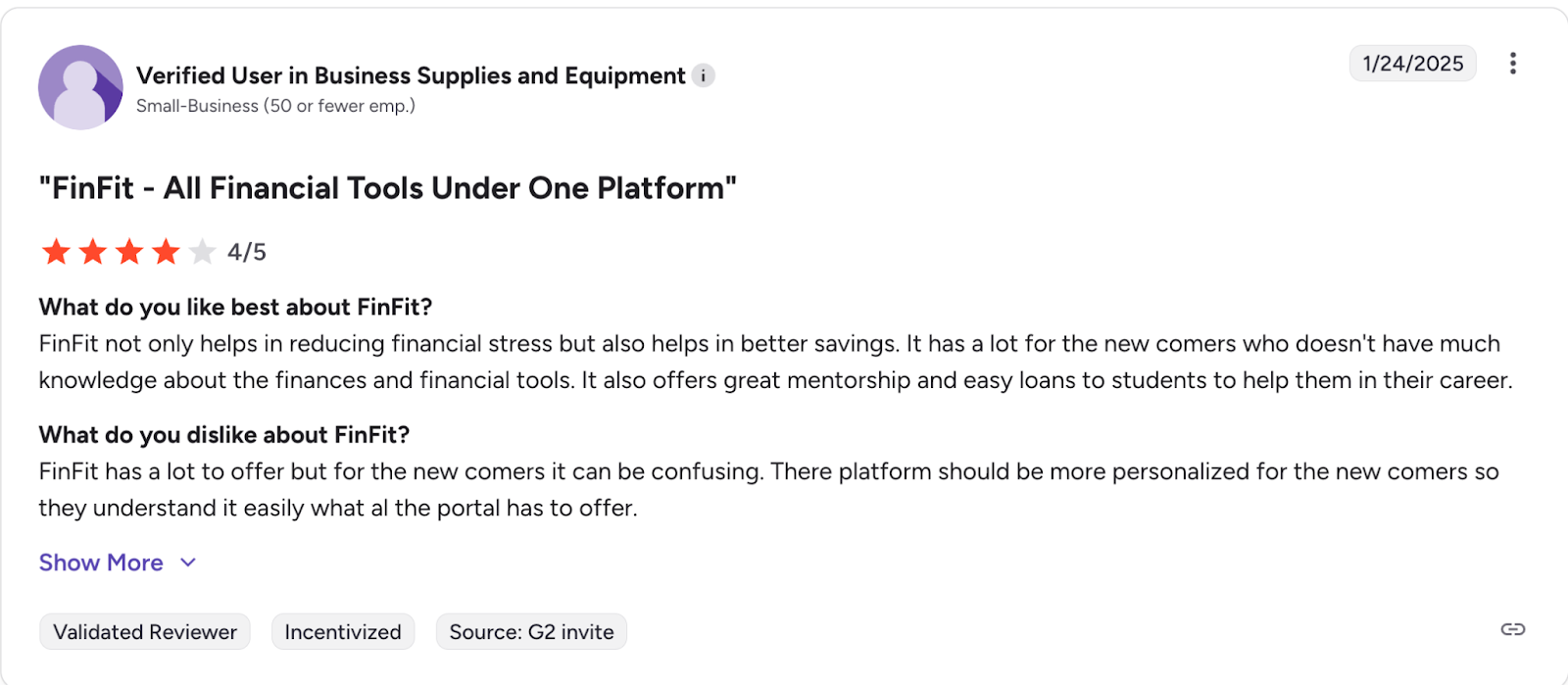

FinFit offers a wide range of tools, but some users find the platform difficult to navigate, particularly those who are newer to managing their finances and need more guided, personalized support to understand what the platform has to offer.

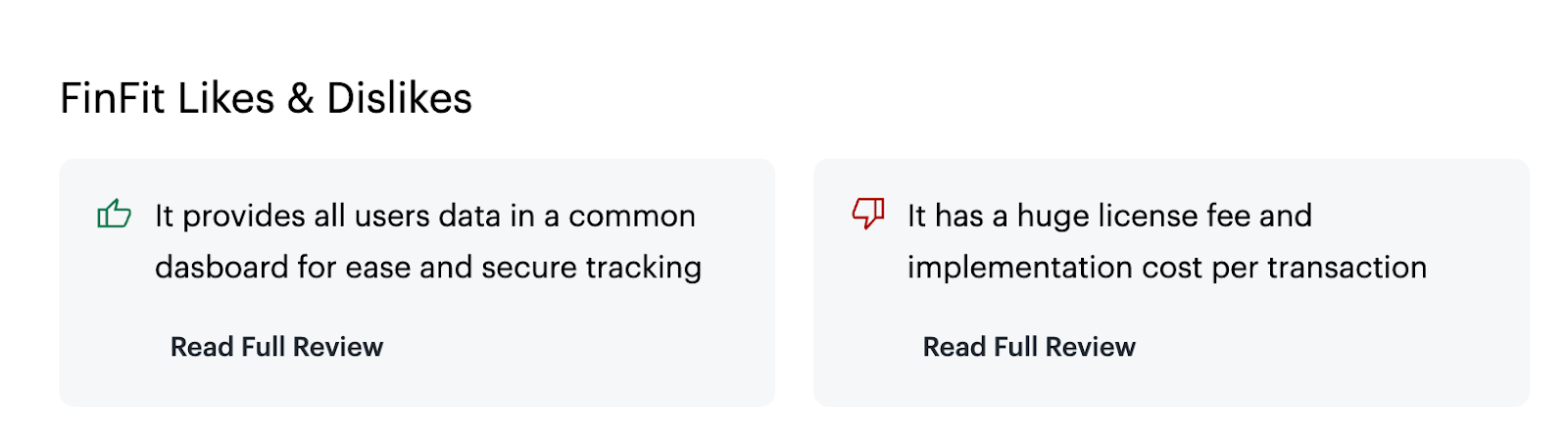

FinFit does not publicly disclose its pricing, and Gartner Peer Insights reviewers flag a "huge license fee and implementation cost per transaction", making it difficult for HR teams to anticipate the true cost before committing.

But the more important cost isn't the one the employer pays. FinFit's personal loans are issued through Celtic Bank, meaning the employer effectively passes the financial burden onto the employee, who is already struggling. That employee is now repaying a lender with interest, out of the same paycheck that was already too small to cover their expenses. The platform's freemium label refers to the employer's cost, not the employee's.

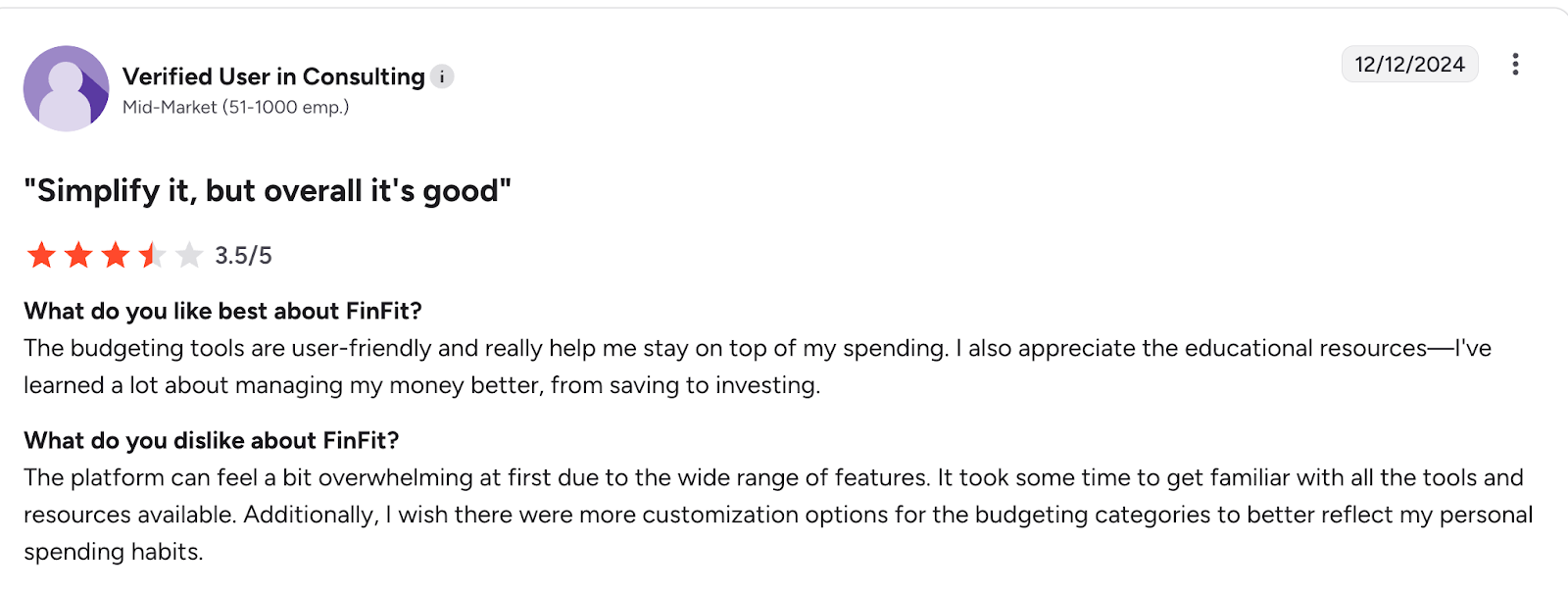

Users report that FinFit's range of tools can feel overwhelming at first, requiring a significant ramp-up period before employees feel comfortable navigating the platform. Several have also noted a desire for more customization, particularly around budgeting categories to make the experience feel more relevant to their individual financial situation.

Whether you're shopping for your first financial wellness benefit or reconsidering FinFit, here's a closer look at the strongest FinFit alternatives for 2026 and how each one measures up.

.png)

Your Money Line is a coaching-first financial wellness benefit that combines certified human coaches with AI-powered tools to help employees make better money decisions across every area of their financial life, building the knowledge, confidence, and habits that create lasting financial stability.

Pros:

Cons

For employees already burned by debt, or by platforms that profit from it, trust is everything. YML is one of the few platforms that can genuinely say: we don't profit from your financial struggle. We only win when you do.

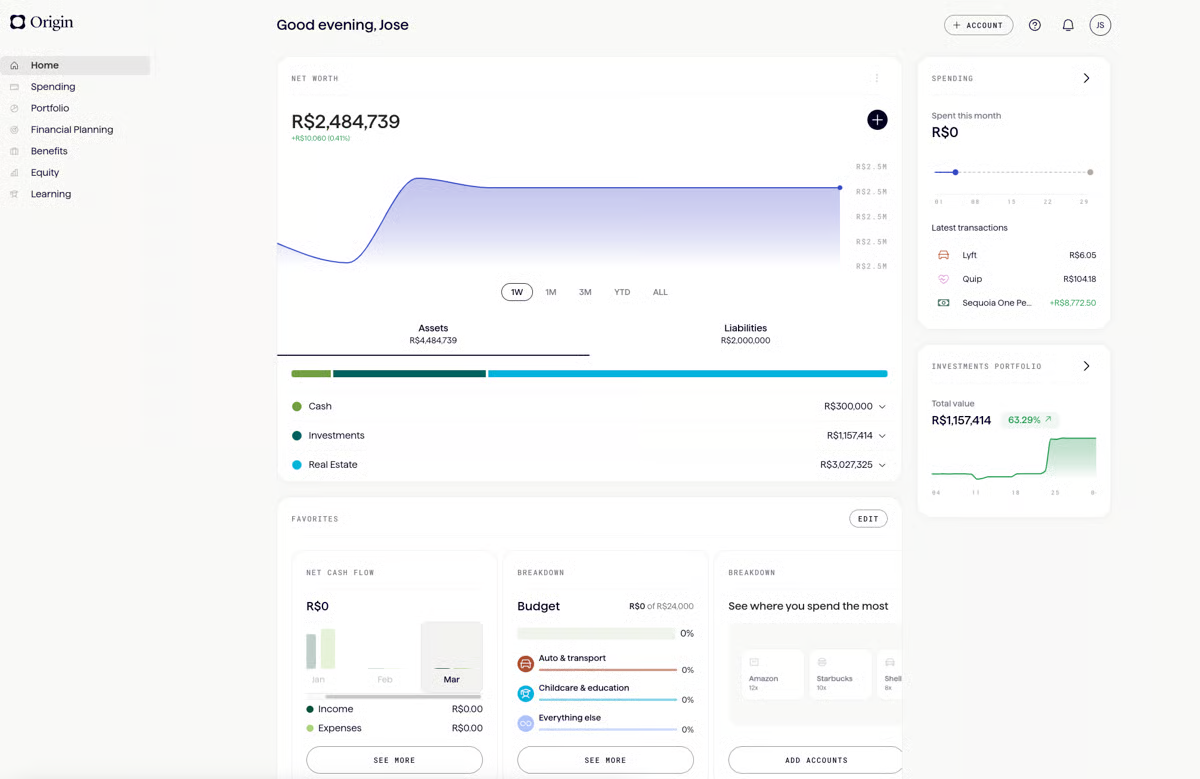

Origin blends AI-driven tools with access to certified financial planners, covering everything from net-worth tracking and tax planning to investing and estate planning. It tends to be a strong fit for organizations with higher-income employees or those navigating more complex financial situations like equity compensation and stock options.

Pros:

Cons:

Bank of America Workplace Benefits is a financial wellness suite that combines digital tools, educational resources, and retirement-focused guidance under one umbrella. Its offerings include Better Money Habits®, a financial education platform built in partnership with Khan Academy, the Life Plan® app for goal setting and budgeting, one-on-one financial coaching through Operation HOPE in select markets, and an integrated suite of retirement, banking, and health benefit accounts for employees.

Pros:

Cons:

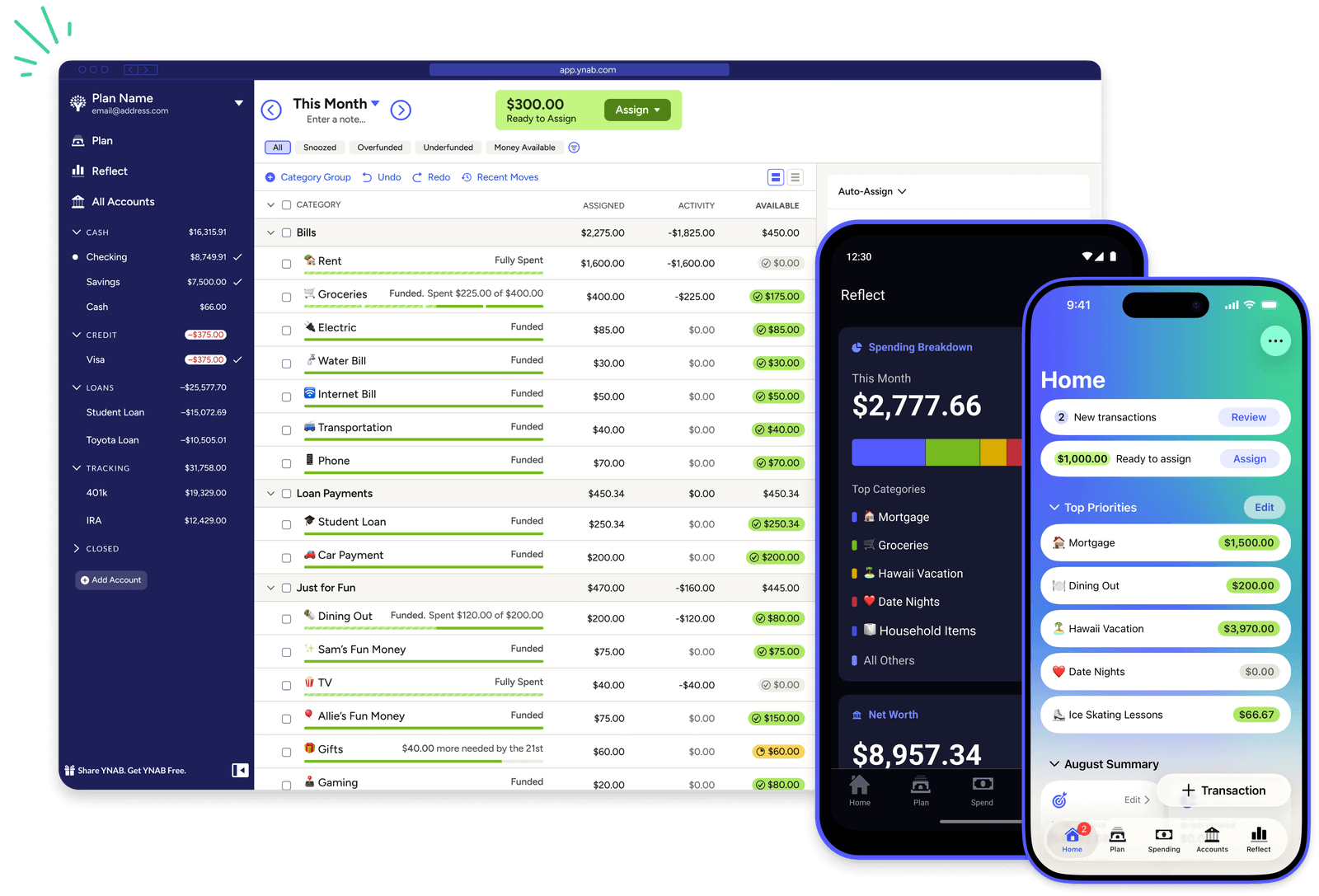

YNAB is a budgeting-focused platform built around a zero-based budgeting philosophy, the idea that every dollar should have a purpose before it's spent. Through hands-on budgeting tools, financial education, and optional coaching, YNAB helps individuals take a more intentional approach to their day-to-day cash flow.

Pros:

Cons:

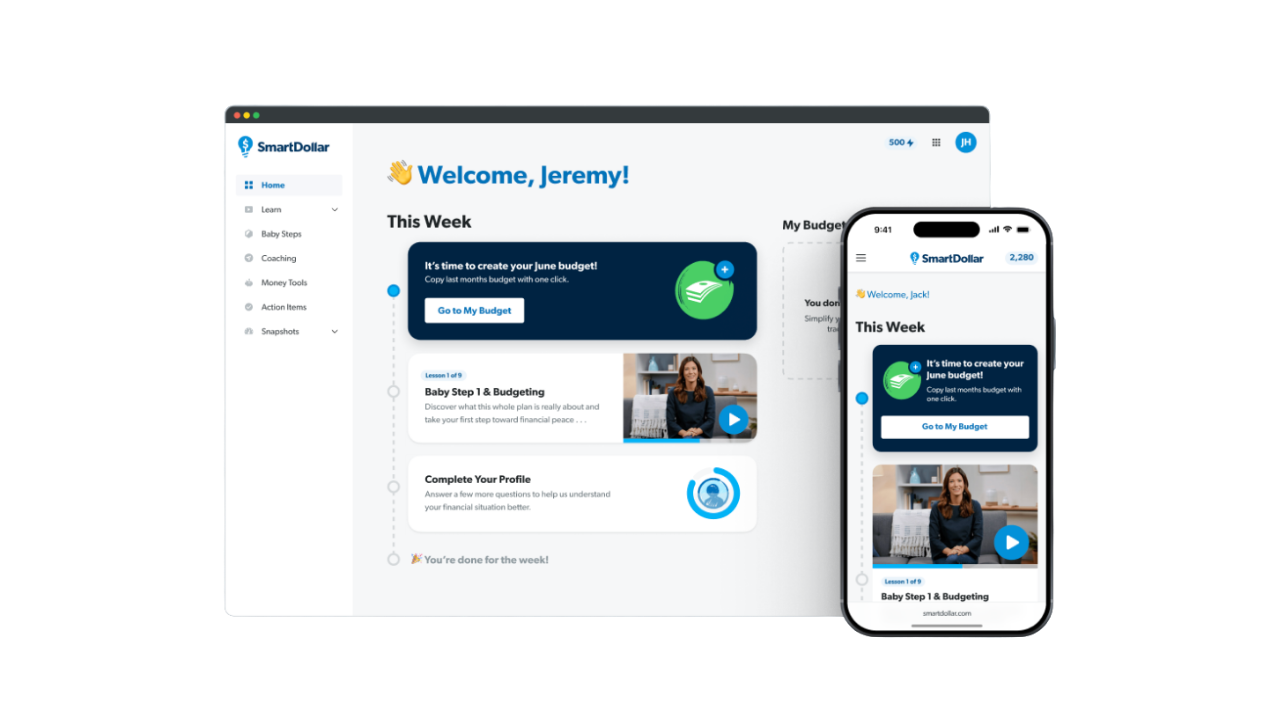

SmartDollar is a well-known name in the financial wellness space, built on the Dave Ramsey brand and a structured, step-by-step curriculum. For organizations whose primary goal is helping employees tackle debt, it offers a familiar and straightforward starting point.

Pros:

Cons:

Not all financial wellness platforms are built the same way, and the right questions can reveal a lot about whether a solution is truly built for your employees or built around a business model. Before signing on with any vendor, consider asking:

Financial wellness benefits have come a long way, but not every platform is built with the same intention. A solution centered on loans and credit access can provide short-term relief, but it doesn't address the root causes of financial stress. Your employees need a trusted resource that helps them budget better, build credit, plan for the future, and make confident money decisions, without anyone profiting from their struggles along the way.

When evaluating your options, the most important questions are simple: Is the guidance truly unbiased? Is there real human support available when employees need it most? Does the platform meet employees where they are regardless of their income, age, or financial starting point?

Your Money Line was built to answer yes to all three. With unlimited access to certified financial coaches, AI-powered tools that personalize the experience at scale, and a model that never profits from employee debt, YML delivers lasting change, not just short-term relief. If you're ready to see what that looks like for your workforce, schedule a demo today.

.png)

.jpg)

.png)