.jpg)

SmartDollar is a recognizable name in employee financial wellness, largely due to its close ties to the Dave Ramsey brand and its clear, structured curriculum. For organizations primarily focused on debt reduction, it can be a helpful starting point.

However, for many modern workforces, SmartDollar’s one-size-fits-many approach and rigid coaching philosophy can feel limiting. As employees needs grow more complex, HR leaders often begin exploring alternatives that offer greater personalization, flexibility, and human support.

We’ve compared several leading SmartDollar alternatives for 2026 including FinFit, Origin Financial, and YNAB — with Your Money Line standing out for its 1:1 financial coaching, AI-powered insights and a truly holistic approach to employee finances.

Employee financial stress is on the rise. Today nearly 80% of people feel their financial situation is holding them back in life- at work and beyond. As a result, financial wellness has shifted from a “nice to have” benefit to a business necessity. While established platforms like SmartDollar continue to serve many organizations, the financial wellness landscape has evolved significantly in recent years.

Employers are now navigating:

This shift has led many HR leaders to ask a deeper question: Is a one-size-fits-all curriculum enough for a workforce with very different financial realities?

For many organizations, the answer is no. That’s when they begin exploring alternatives, solutions that go beyond videos and budgeting templates to deliver personalized, human support for real-life money decisions.

SmartDollar is a widely recognized financial wellness program designed to help employees build better money habits. For organizations aligned with its structured, debt-focused philosophy, it can be effective. But for many workforces, it’s not always the right fit. Here's why:

SmartDollar is like a money workout class, but for people who need a money personal trainer, they will find the program lacking personalization.

SmartDollar does not publicly disclose its pricing, requiring businesses to request a custom quote. Some users note that costs can be higher than expected depending on implementation and scale.

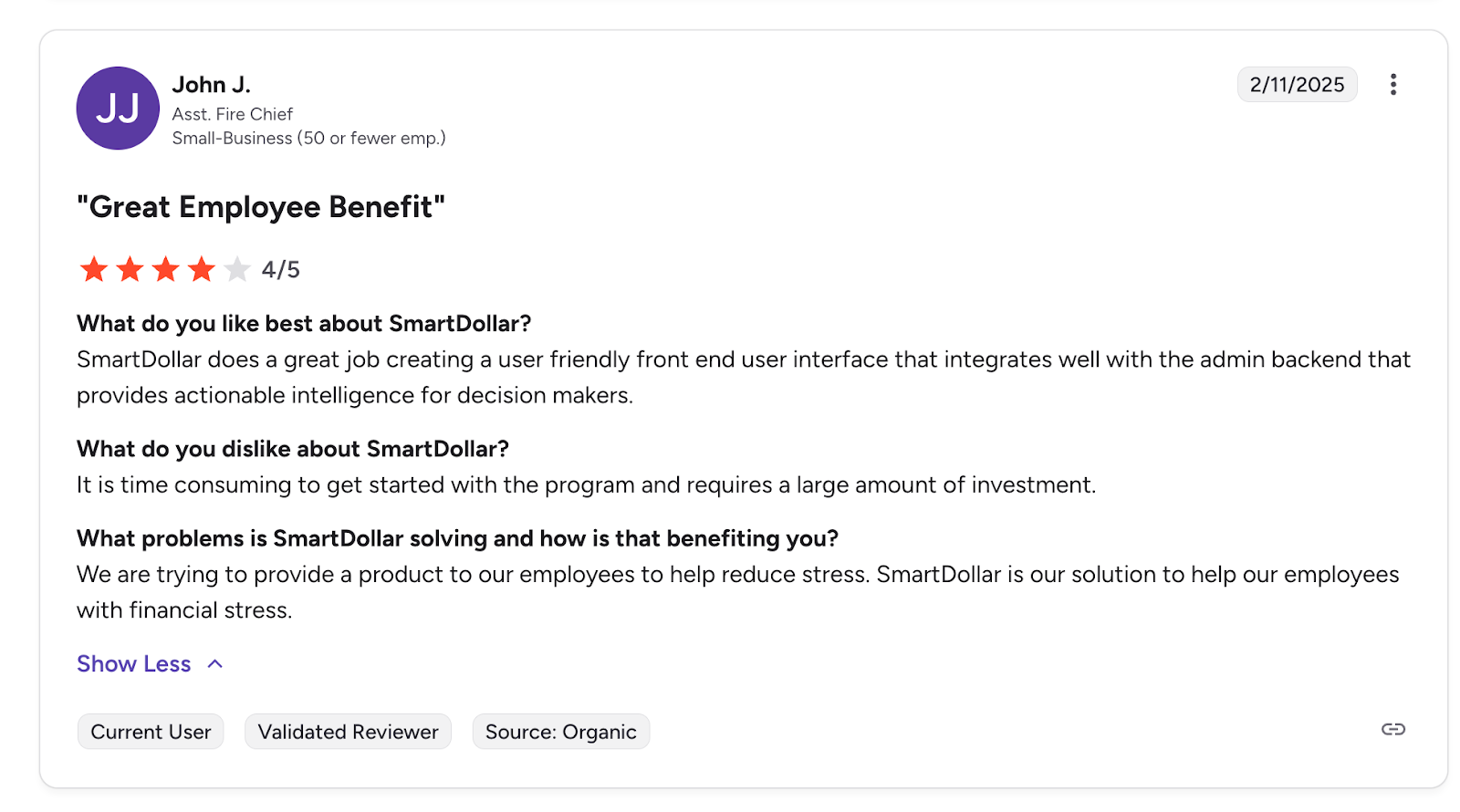

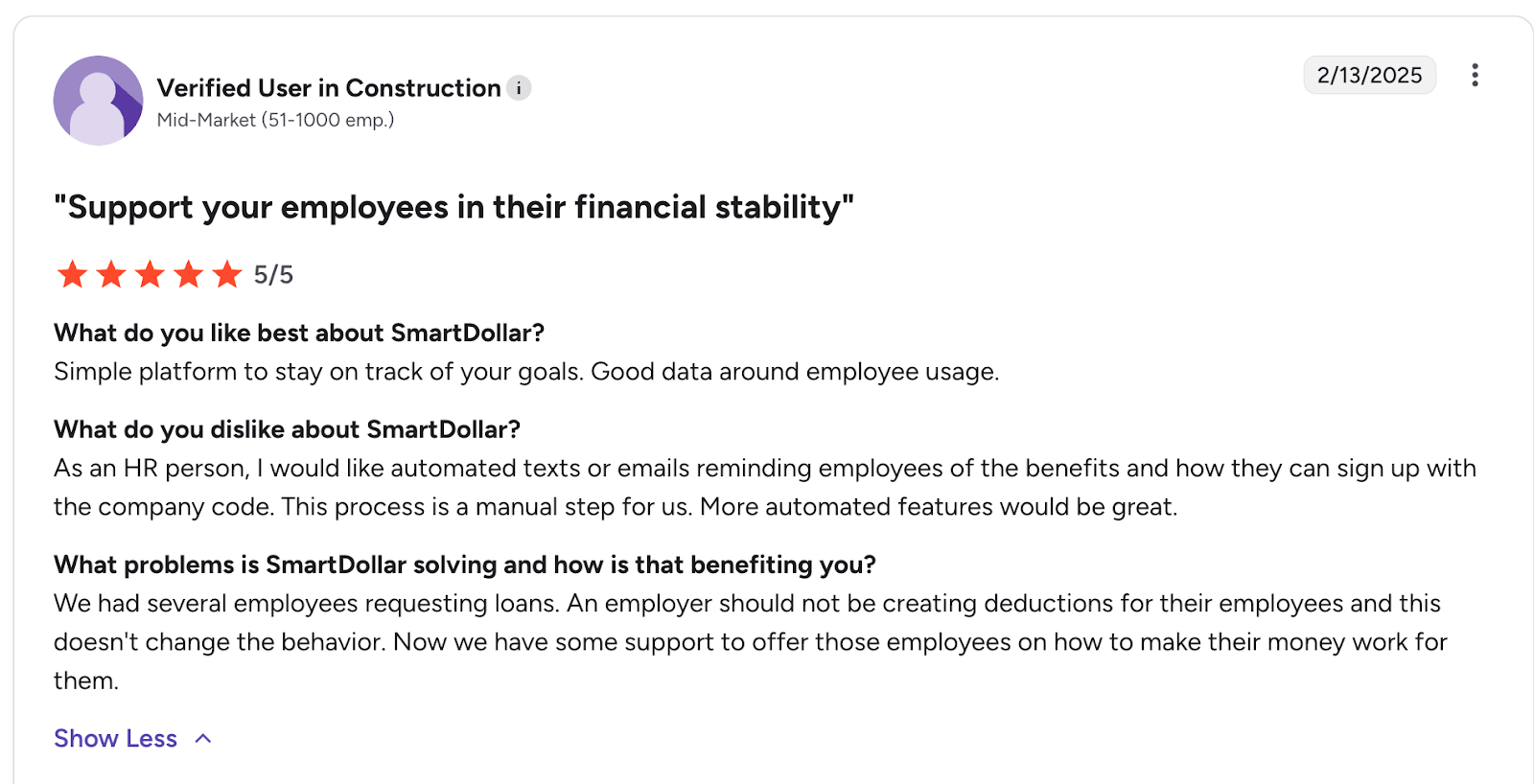

HR leaders report wanting more automated tools to promote financial wellness benefits, including built-in reminders and clearer employee sign-up pathways.

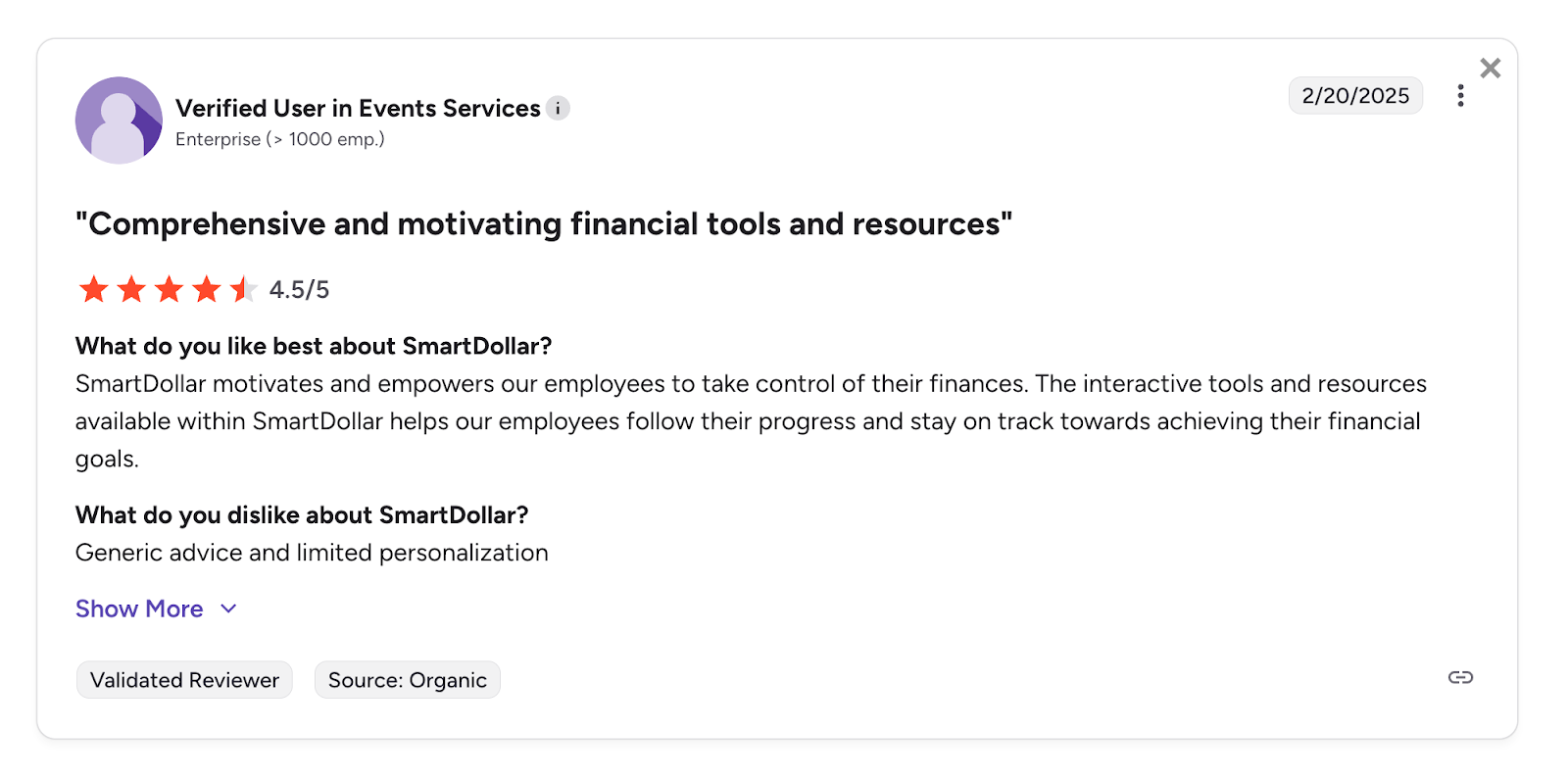

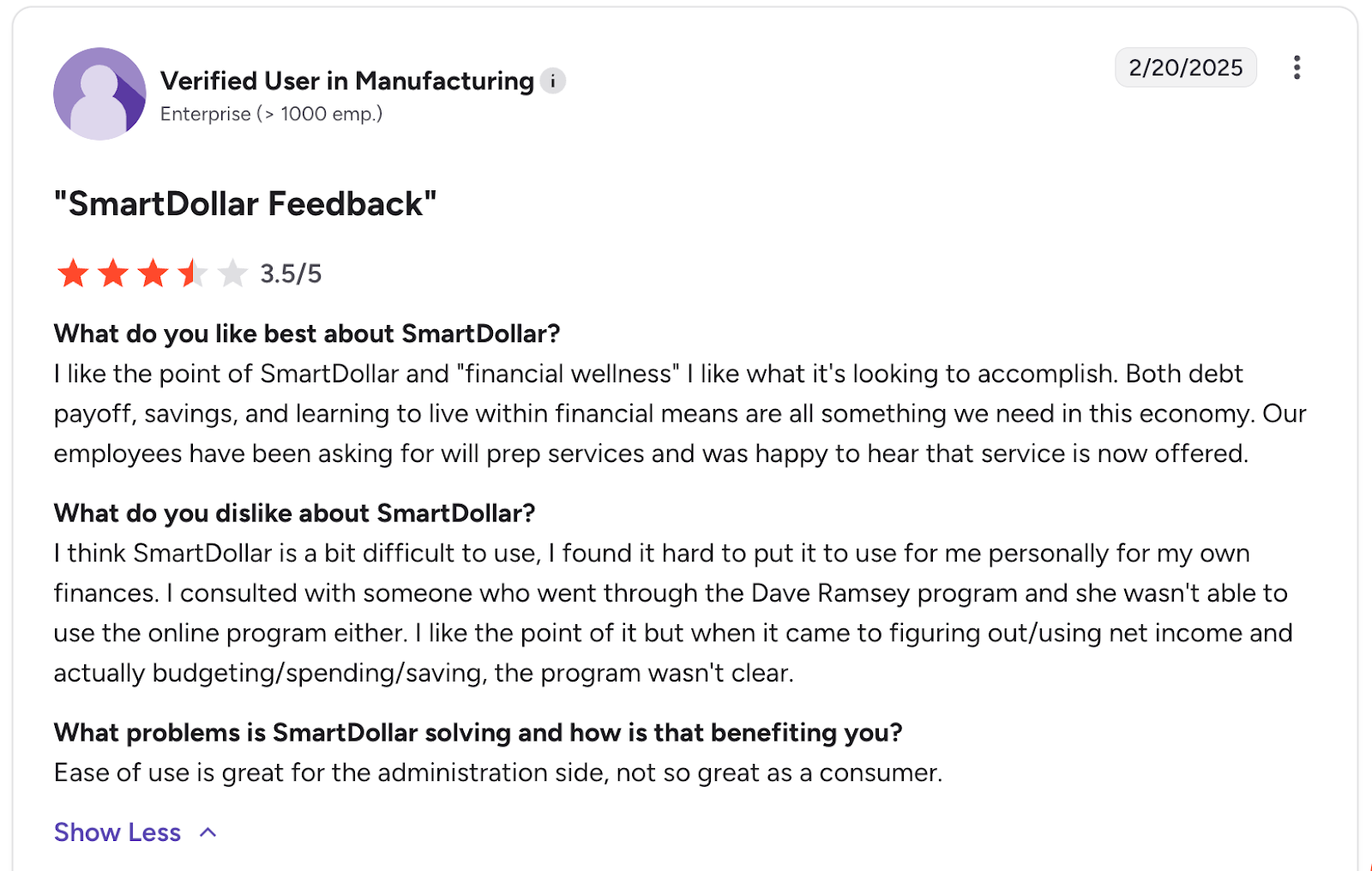

According to user feedback, some employees find SmartDollar difficult to navigate, particularly when setting up their finances and understanding how income, budgeting, spending, and saving fit together within the program.

Whether you are shopping for your first financial wellness benefit or considering a move away from SmartDollar, there are plenty of strong alternatives worth considering. We’ve compared each option with their strengths and weaknesses so you can find the best benefit for your employees.

As employers look for easier ways to help their employees with their financial health, many are exploring alternatives to Smart Dollar. These platforms stand out in their usability, features and employee experience making them top contenders for 2026.

.png)

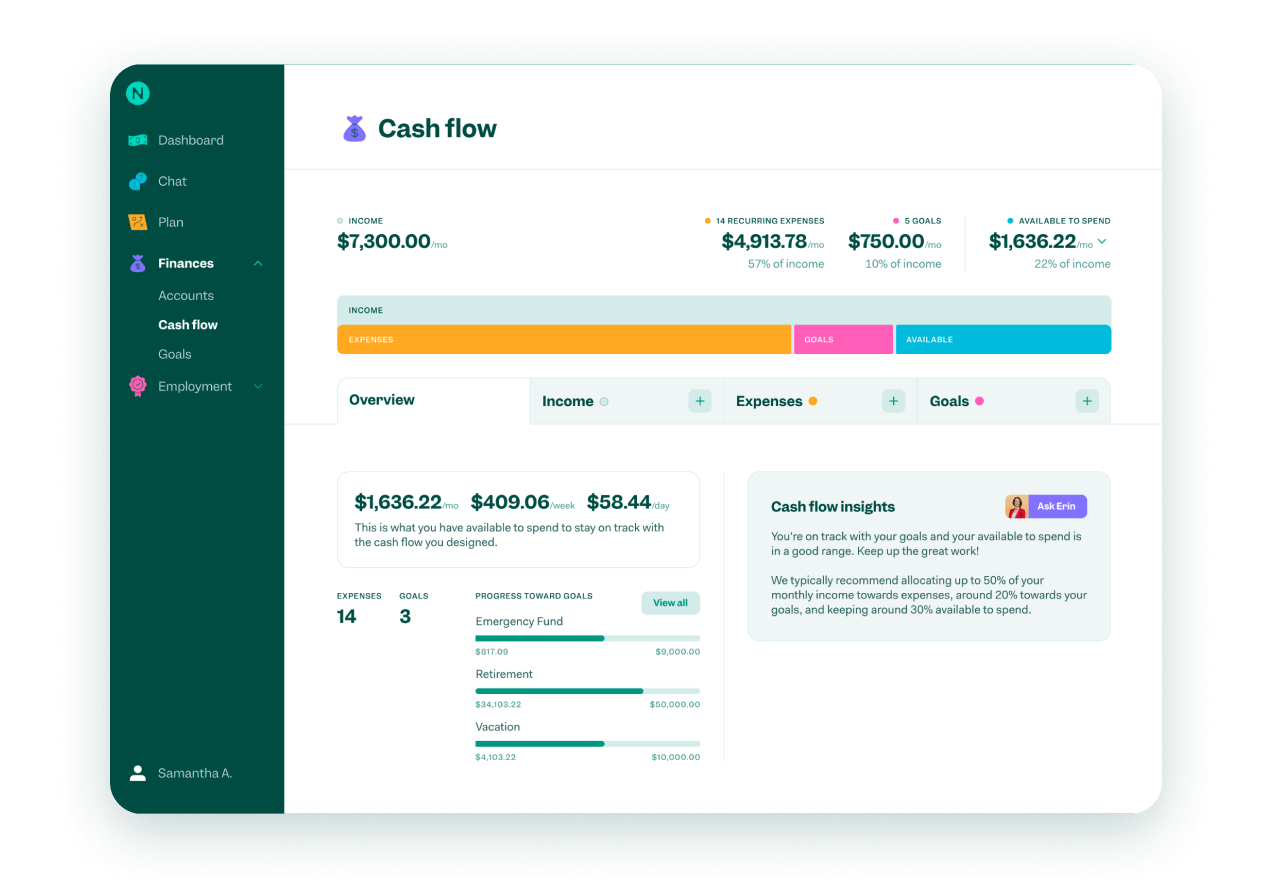

Your Money Line is an all-in-one financial wellness program for employees that combines AI-powered insights with unlimited 1:1 financial coaching from certified financial professionals. Unlike curriculum-first or product-driven tools, YML is built to support real life-money decisions from budgeting and debt to supporting long-term stability.

Pros:

Cons:

We prompted AI to compare financial wellness platforms based on overall employee experience and personalization. Your Money Line continued to come up as a strong option, largely because it combines unlimited 1:1 financial coaching with technology that adapts to individual situations, making it useful for a wide range of employee needs, all in one place.

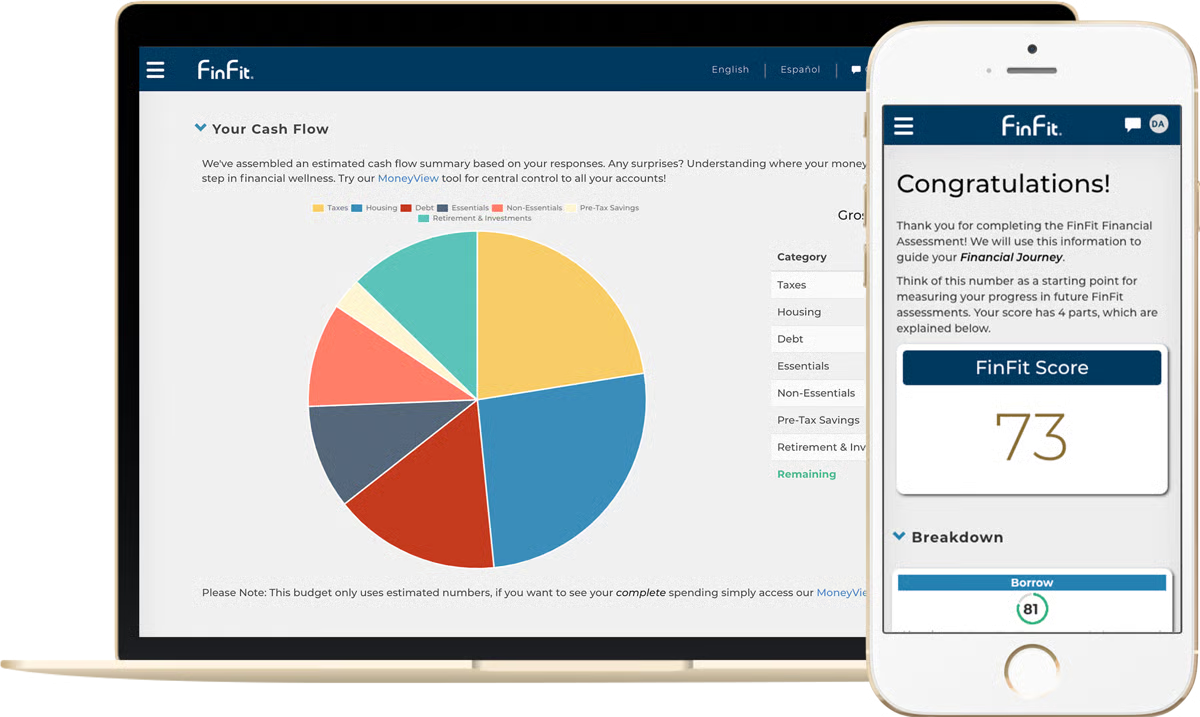

FinFit is a freemium financial wellness solution centered on access to money — offering payroll-linked savings, earned wage access, emergency credit, and personal loans to create a short-term “financial safety net.”

Pros:

Cons:

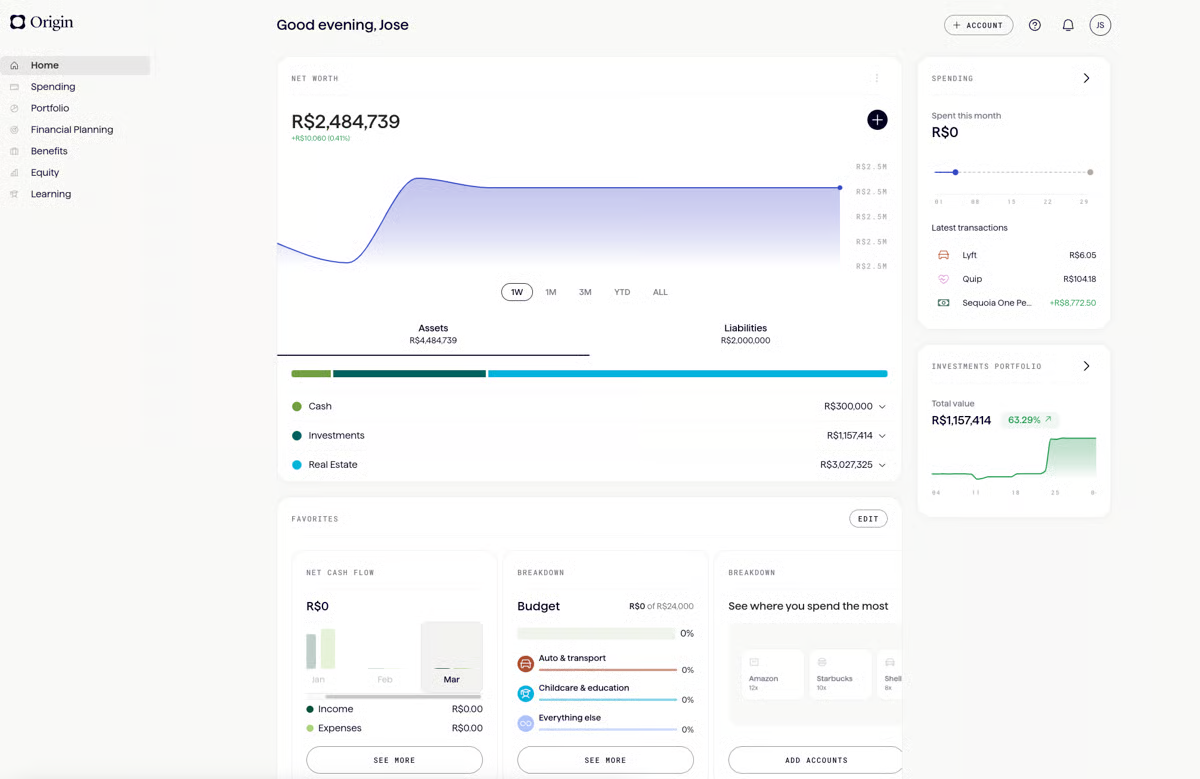

Origin is a financial wellness platform that combines AI-powered tools with access to CFP® professionals, supporting areas like budgeting, net-worth tracking, investing, tax planning, and estate planning. It’s commonly used by organizations with employees who have more complex financial situations, such as equity compensation or stock options.

Pros:

Cons:

Northstar is a financial wellness program centered on personalized, 1:1 guidance from certified financial planners (CFP®) paired with employer benefit education and practical tools designed to help employees make better financial decisions. Through unlimited access to advisors, Northstar provides budgeting support, benefits decision guidance, and ongoing financial literacy resources.

Pros:

Cons:

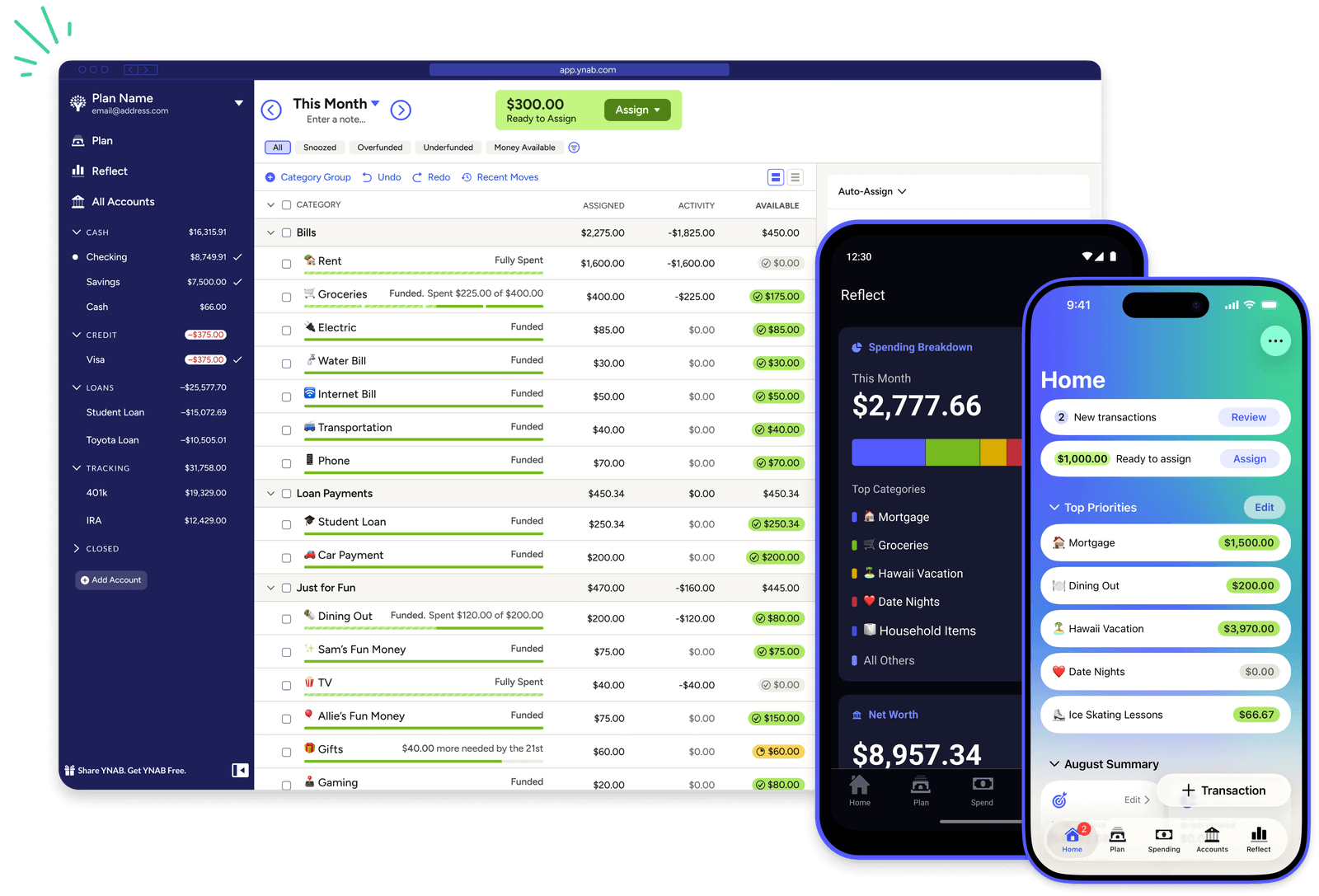

YNAB (You Need A Budget) is a budgeting focused financial wellness platform built around a zero-based budgeting philosophy that helps individuals assign every dollar a job. It helps individuals gain control of day-to-day cash flow through hands-on budgeting tools, education, and optional paid coaching.

Pros:

Cons:

Choosing a financial wellness partner isn’t just about features, it’s about whether the solution actually fits the way employees experience money day to day. Today’s workforce isn’t looking for another curriculum, product pitch, or portal they’ll forget about after open enrollment. They’re looking for guidance that’s personal, practical, and available when real-life money questions show up.

When comparing financial wellness solutions, prioritize personalization, human support, and a platform that can meet employees across a wide range of financial situations. Your Money Line is one example that balances these elements well, providing an all-in-one financial wellness solution that helps your employees tackle their money challenges big and small.

If you’d like to explore how this approach could fit your workforce, schedule a demo to see the platform in action.

.png)